1x

1xIn all likelihood, you are already an expert in embedded finance – you just don’t realize it.

Buying a new book or pair of sneakers through an e-commerce platform like Amazon? You just used embedded finance. Reimbursing a friend for a concert ticket with a peer-to-peer payment through your digital wallet? Again, you just used embedded finance. Paying for a journey through a ride-hailing app, investing in cryptocurrency, or booking a minibreak on a buy-now-pay-later deal? Chances are, you have embedded finance to thank for that, too.

Embedded finance is everywhere, so interwoven with modern life that we hardly notice when we are interacting with it.

The numbers tell their own story: A story of a genuinely transformational financial tool undergoing mass adoption due to its irresistible usefulness.

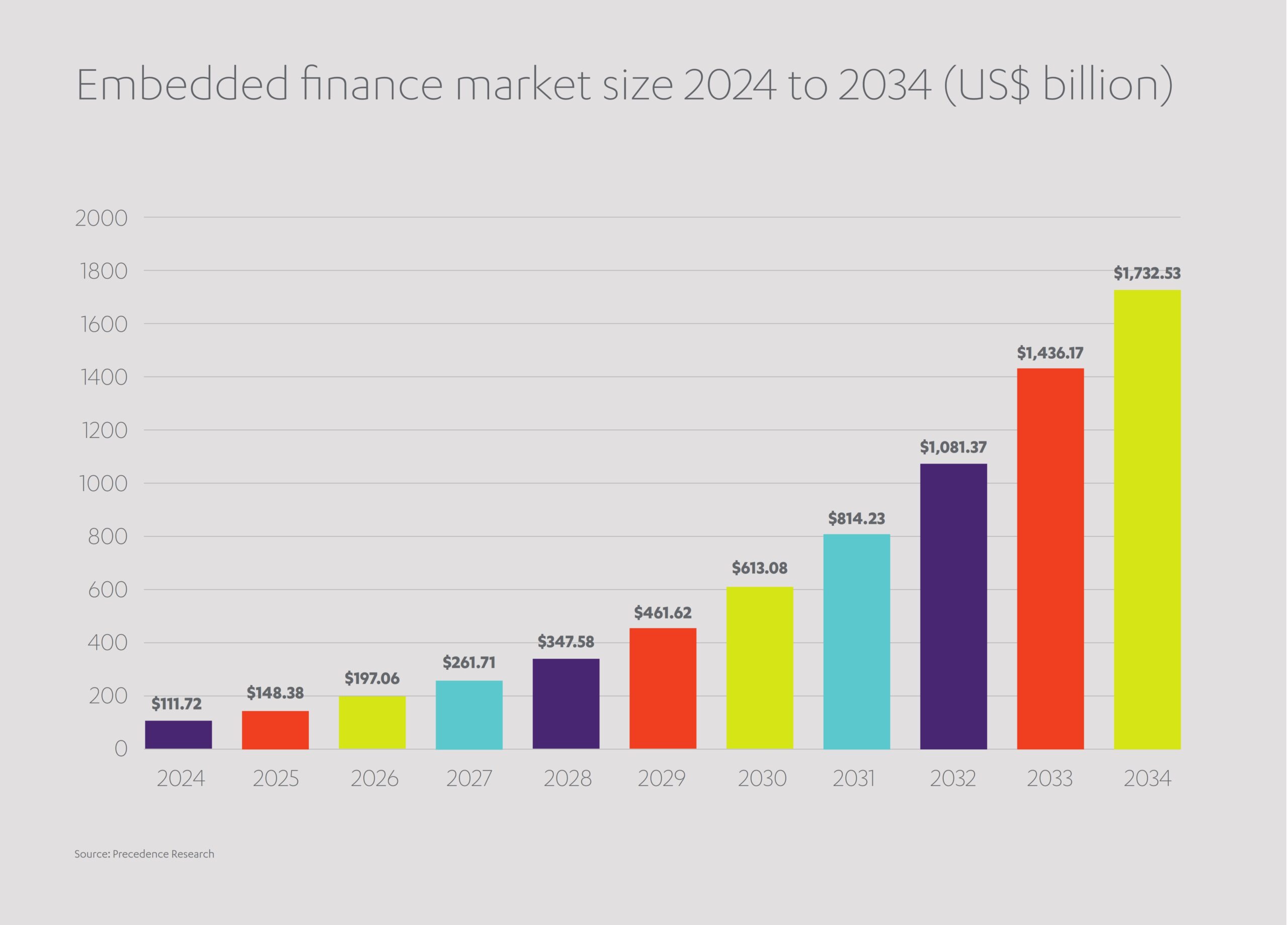

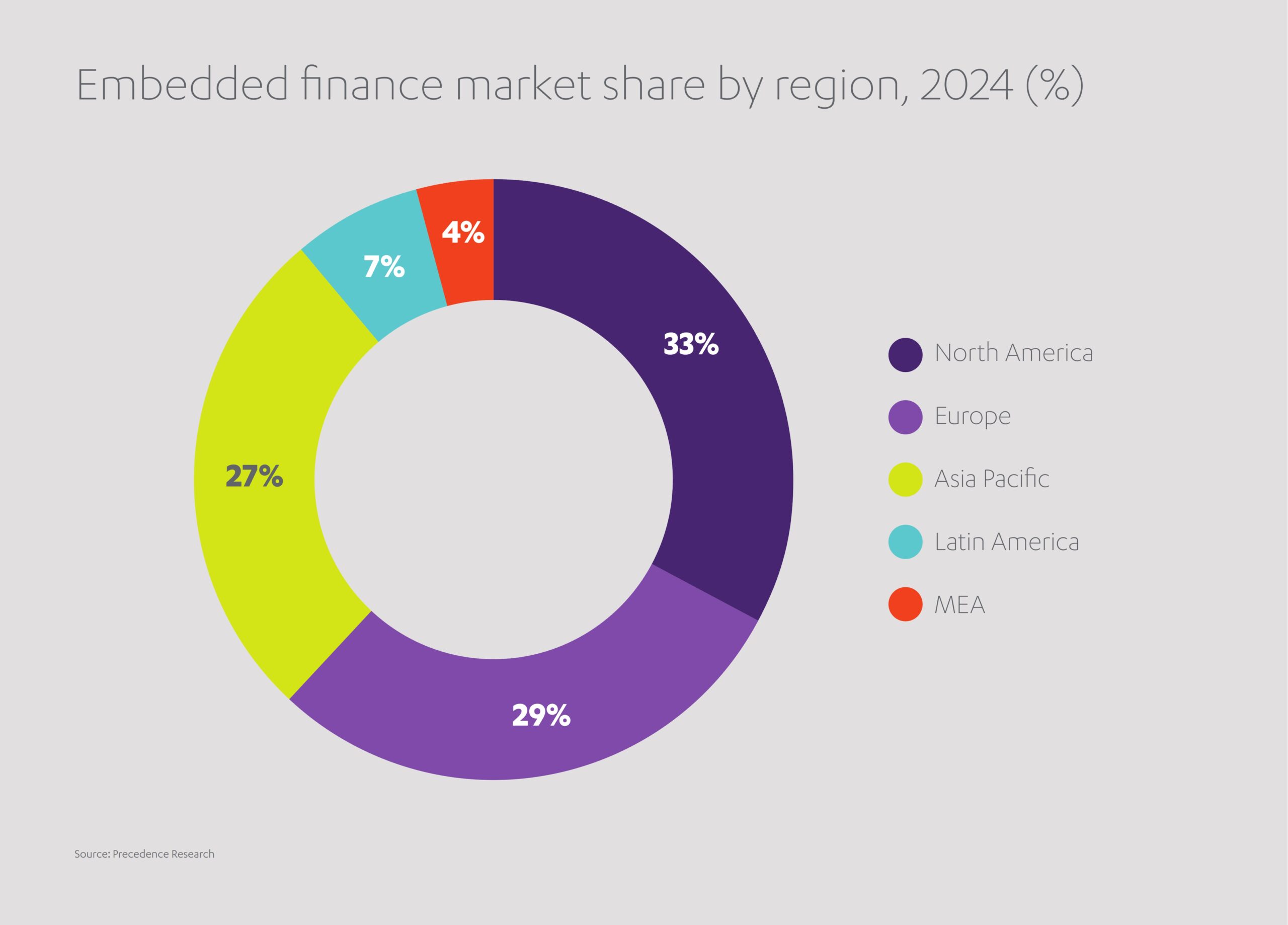

The embedded finance market was valued at US$ 111 billion worldwide as of 2024, and with rapid growth is tipped to reach US$ 613 billion by 2030.[1] The total amount of cash funneled through embedded finance technology crossed the US$ 2.5 trillion milestone at the start of the decade and has risen swiftly ever since, with transactions expected to hit US$ 6.5 trillion by the end of 2025.[2] The trend is global: In the MENA region, for instance, an embedded finance market valued at US$ 11.2 billion in 2024, is predicted to mushroom to US$ 37.7 billion by 2029.[3]

Almost all of us benefit from the streamlined efficiency of embedded finance, but do many of us actually understand its intricacies? As a multi-trillion dollar financial tool, it is worth diving deeper into what the term actually means and how the technology that underpins it works.

How important is API technology to embedded finance?

‘Embedded finance’ refers to the incorporation of everyday financial amenities – banking services, insurance, payments or loans – into nonfinancial websites and apps. In essence, it allows customers to conduct their financial transactions quickly and simply through a business’s own online platform, instead of navigating away (or being redirected) to a bank or financial provider.

It provides a safe, prompt method of making a transaction, setting up a payment plan, agreeing a loan or sourcing insurance, without the logistical headache of visiting multiple sites or applying for separate credit agreements. Just as seamlessly as they handle payments, APIs are also powering embedded lending — from SME credit lines offered within e-commerce platforms to instant personal loans accessed through consumer apps. Embedded finance is a hallmark of a time-poor, one-click world, one which eases the wheels of commerce and gives consumers quick access to the products and services they need.

That all makes sense in principle – so how exactly does it work? Clearly, e-commerce platforms are not all expanding their operational remits to encompass financial services. Amazon has no wish to become a bank; your local car dealer lacks the skills to become a lender; travel firms don’t want to become payment plan providers. How then can they offer these services without shouldering the massive technical and regulatory burdens of the financial sector?

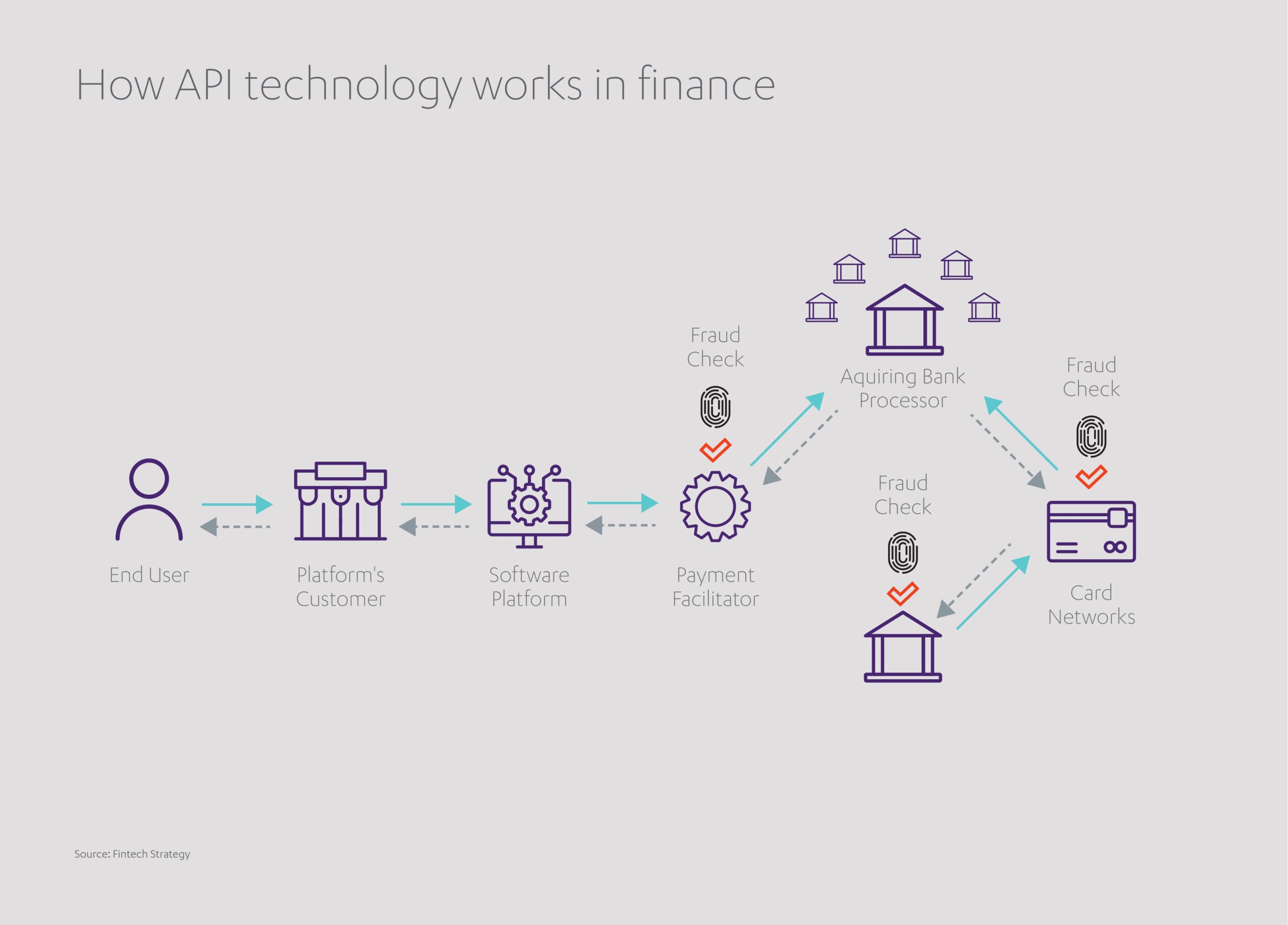

The answer is through Application Programming Interfaces, or APIs, managed by an external banking-as-a-service partner. An API is the connective tissue allowing e-commerce platforms to integrate basic banking services into their user experience.

APIs are best imagined as ‘software intermediaries’ enabling secure data exchanges between financial institutions and customer-facing enterprises, such as retailers or investment platforms. Typically, a five-step API process involves:

- a request (a customer making a query via an online retailer)

- an authentication (the API confirming the legitimacy of the request to access data)

- data retrieval (downloading the necessary data from the bank or lender)

- formatting (translating that data into a standardized form interpretable by third-party apps)

- response (delivering the formatted data to the customer).

Conveniently, shoppers only need link their bank account to an external platform once, and then all subsequent purchases are fast and effortless.

Such a system offers multiple benefits. It allows different sectors to interact seamlessly, all while maintaining privacy protocols. The data accessed is live, reflecting second-by-second fluctuations in bank accounts or stock markets. It is also secure, demanding multi-factor authentications such as passwords, biometric data and one-time codes. Encryption ensures communications remain confidential, while regulatory compliance offers reputational credibility. APIs in Europe, for example, abide by Payment Card Industry Data Security Standard (PCI DSS) for payments and General Data Protection Regulation (GDPR) for data protection.

APIs, in other words, allow nonfinancial companies to communicate harmoniously with financial platforms. The benefits, according to global business advisory PWC, do not end there.[4] Embedded finance can also:

- Helps companies find and retain customers by maximizing convenience and reducing friction.

- Creates new revenue streams with existing users by expanding the range of transactions and finance schemes on offer.

- Equips companies with valuable data on customer preferences and behaviors, enabling the creation of tailored products and services.

- Encourages customer loyalty by providing a one-stop-shop for all their transactional needs, without the risk of attention pivoting to third-party providers.

- Enable businesses to move beyond transactions to build personalized financial journeys, tailoring credit, savings, or insurance offers in real-time based on customer behavior.

Thanks to embedded finance, lenders, technology platforms and startups are busy collaborating on a new wave of financial technology (fintech) partnerships heralding hassle-free, fully-integrated financial services. What will this new API-driven ecosystem look like?

How could partnerships and AI boost embedded finance?

Embedded finance is at the vanguard of fintech innovation and will transform the future delivery of financial services, according to the World Economic Forum[5]. Banks will interact with fewer customers directly, but will be far from obsolete. APIs may govern payments, loans and insurances, but do not themselves retain or have access to funds – banks remain the repositories of wealth and investment.

Banks offer size, a ‘too big to fail’ structure, scalability and longstanding reputational integrity. Fintech operators, on the other hand, are quicker to embrace innovation, can react more nimbly to shifting trends and are not so wedded to outdated technology. Partnerships, therefore, are emerging as the prime solution for our bold new age of embedded finance.

Quantix, the fintech arm of UAE-based technology group Astra Tech, revealed in December 2024 that it had secured US$ 500 million in financing from American multinational bank Citigroup[6]. The investment enables Quantix to expand its CashNow consumer lending platform to overlooked communities such as SMEs and gig workers. Citigroup, for its part, gets to penetrate the burgeoning embedded finance sector and diversify its portfolio. As a collaboration, it signifies the UAE’s largest fintech deal to date.[7]

Similarly, international banking giant HSBC has partnered with San Francisco-based B2B fintech platform Tradeshift on a new venture named SemFi[8]. SemFi helps e-commerce sellers, often sole traders or SMEs, receive payments faster by having invoices paid early by HSBC. It aims to provide new lines of credit to a wider range of customers by analyzing transaction histories and directly accessing sellers’ accounting tools.

Likewise, recent partnerships between US bank JPMorgan Chase and finance fintech Gusto, and UK bank NatWest and embedded finance innovator Vodeno, enable customers to embed payroll services within their systems and add payment options to products.[9]

Such collaborations, along with others in the pipeline, could help empower those segments of society traditionally excluded from banking services, all while improving financial literacy and democratizing access to investment.

In emerging markets, embedded finance offers SMEs access to working capital, transforming supply chain finance into a real-time, digital service embedded directly into procurement and trade platforms.

Breakthroughs in AI will only hasten this journey. AI will make embedded finance faster by allowing transactions in real-time. Tailoring its interface around the individual, AI will also make buying products, paying invoices or handling investments far more intuitive. With its unprecedented processing power and advanced algorithms, AI will also be able to pinpoint any illicit activity, making embedded finance the safest choice for future transactions. In another win for financial inclusivity, AI-powered credit scoring could make loans available to people lacking traditional credit histories, potentially narrowing the finance gap between ‘haves’ and ‘have nots’.

Indeed, with some of the more exciting innovations happening within the MENA region, embedded finance could eventually help emerging markets compete on a more level playing field with their mature market rivals.

How advanced is the MENA region in embedded finance?

Although currently the size of the market in the MENA region is small, it boasts a promising embedded finance ecosystem with the potential to rapidly scale-up. In fact, with the Middle East serving as a hotbed of tech innovation, embedded finance is projected to grow twice as quickly in MENA this decade as in the rest of the world.[10]

This is partly driven by ambitious investments from telecommunications companies, retailers and tech startups, but also by MENA’s embrace of an ‘open banking’ culture. Open banking, in which financial institutions allow third-party developers access to their data, is a prerequisite for embedded finance. At state level it has received major support via legislation such as Bahrain’s Open Banking Framework, the UAE’s Financial Infrastructure Transformation Program and Saudi Arabia’s Open Banking Policy.

Businesses in MENA have taken note and invested accordingly. Notable ventures include buy-now-pay-later (BNPL) startups, integrated digital banking platforms, and a raft of new insurance technologies, where embedded models are reshaping access, from travel protection at the point of booking, to micro-insurance for health, mobility, and devices embedded into everyday purchases. One high profile deal, between ride-hailing app Uber and insurance giant Axa, offers bespoke insurance plans for Saudi Arabia’s taxi and delivery sector, plus medical and legal coverage for all customers using the Uber app.[11] More recently, the Saudi Telecom Company (STC) joined forces with BNPL platform Tamara to offer payment schedules for customers of STC’s electronics and accessories, massively broadening its potential customer base[12].

Embedded finance is gaining particular momentum in the UAE. The sector is expecting a compound annual growth rate (CAGR) of 28.6% between now and 2029 thanks to a sharp rise in e-commerce and robust investment in digital infrastructure.[13] Dubai-based Careem Pay is continually expanding its international remittance services, this year adding an extra 18 European countries to its approved transfer corridors[14]. Online marketplace Noon, meanwhile, also headquartered in Dubai, has launched digital wallet Noon Pay. Noon allows users to add money to their balances using a Visa or Mastercard via a secure app on their iOS or Android cellphones. With one eye on the future, the UAE’s Young Investor Program is equipping the entrepreneurs of tomorrow with all the financial and digital skills needed to become savvy operators in embedded finance[15]. In highlighting the spirit of ‘coopetition’ (a fusion of competition and cooperation) in the UAE’s finance sector, the World Economic Forum cites the country as a potential global hub for fintech in the coming decades.[16]

The financial services sector businesses within the Abdul Latif Jameel network are similarly immersed in several embedded finance initiatives within the region.

- In 2023, Abdul Latif Jameel Finance in Saudi Arabia launched its Jameel Business app, the first digital platform dedicated to financing SMEs in the country, offering up to SAR 15m in credit.

- Abdul Latif Jameel Finance also unveiled its personal loan app in 2022, Cash Jameel. One of the first products of its kind in Saudi Arabia, Cash Jameel allows individuals to apply for personal loans between SAR 10,000 and SAR 20,000 each. The user-friendly app processes bids within minutes and agreements can be signed digitally, avoiding time-consuming paperwork.

- Similarly, in Turkey, ALJ Finans has operated the award-winning ALJPay credit application app since 2017. The app allows motorists to search for new vehicles by specifying their preferred manufacturers, including embedded financial services for end customers, dealerships and repayment schedules, with e-contracts emailed out in less than five minutes.

- In the UAE, meanwhile, JIMCO’s technology fund is an investor in BNPL provider Tabby, which has been integrated with major global brands including Ikea and Nike. Tabby allows customers to split debt into multiple interest-free payments and earn cashback at chosen retailers.

- JIMCO has also invested in Turkish fintech start-up Figopara, helping businesses make ends meet by extending working capital. Reimagining supply chain finance for the demands of the modern world, it enables businesses to lengthen payment terms while simultaneously allowing suppliers to be paid early – a win-win for both parties.

- UAE-based tmam has received JIMCO backing to accelerate development of its ‘spend and expense management’ platform for small businesses and entrepreneurs. tmam technology saves time and helps avoid costly errors by allowing real-time monitoring of spending and expenses, together with a smart corporate card for greater cash control.

- In addition, JIMCO has also invested in Ziina, a financial platform offering businesses and consumers across the UAE instant money transfers, QR code payments and secure payment gateways. Ziina already has more than 50,000 active users and will soon launch its own ZiiCard, providing customers with instant access to their digital wallet balances.

It’s not just about facilitating payments. These initiatives – among many others – show that embedded lending, not only BNPL but also SME financing and personal loans, is becoming a mainstream feature of the region’s financial landscape, opening new lines of credit for SMEs, gig workers, and consumers, and reshaping how financial access is delivered.

With embedded finance making headlines around the world, and in particular within the Middle East, are there any obstacles to a wider roll-out – and what should public and private sector players be doing to prepare for its rising profile?

What’s the future for embedded finance?

The foundations have been laid for a vibrant international system of embedded finance technologies, but global adoption is not assured. Developers must create new iterations of APIs even more versatile than the existing generation, so that any platform can quickly and simply introduce financial services to its user interface.

High costs associated with purchasing new API technology, and a perceived lack of in-house skills, are delaying many businesses from making the leap.

Complex and sometimes contradictory regulations in different countries could also impede progress. Tech firms, banks and retailers require clear and consistent legislation to give them the confidence to invest adventurously.

Among the potential global customer base, not enough individuals or small businesses are yet aware of the benefits – or even the existence – of embedded finance products. Like any relatively young technology, concerns persist around trust and security.

Fortunately, the solutions to these hurdles are clear: Generous investment in new API research, likely from a mixture of public and private sources; a unified approach to regulation, ensuring technical and legal challenges are consistent wherever in the world an online transaction is triggered; and more effective customer communication strategies to build faith among the tech-wary. Economies of scale will, in time, lower the technological cost of entry.

As for businesses currently redirecting customers to third-party websites to conclude their payments? These companies could choose to invest in digital infrastructure and data architecture, ensuring future transactions are managed internally while also opening up new revenue streams.

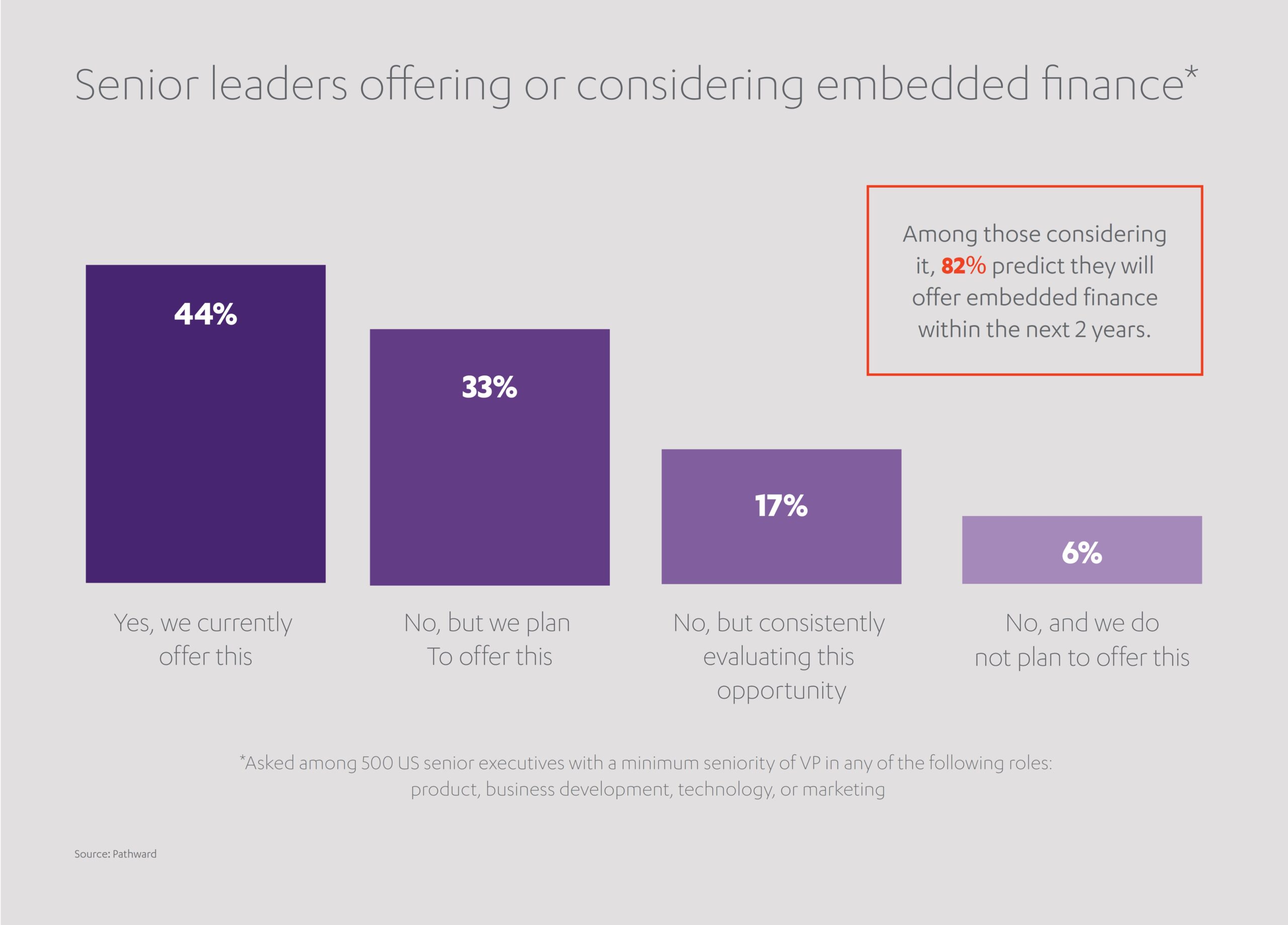

Embedded finance is already upon us. Its merger with our everyday apps and websites will only accelerate. Some 77% of senior executives questioned in 2024 said their businesses already incorporated embedded finance or were considering implementing it soon. [17] On a cautionary note, the same survey revealed that four-in-five corporate leaders admitted they had somewhat, or significantly, underestimated the complexity of introducing it into their business models. Preparation is therefore key.

In a time-pressed world, convenience is king. As such, API-driven technology is destined to become an invisible partner in our daily lives. Embedded finance is about creating ecosystems where financial services become a natural layer of digital life, from mobility to education. Offering greater efficiency for individuals, and new revenue opportunities for businesses, it demonstrates what can be achieved when innovation is unleashed and the worlds of technology and commerce collide.

[1] https://www.precedenceresearch.com/embedded-finance-market

[2] https://www.marqeta.com/blog/real-world-examples-of-embedded-finance

[3] https://www.weforum.org/stories/2025/04/embedded-finance-disruptive-force-financial-institutions/

[4] https://www.pwc.com/gx/en/issues/technology/tech-translated-embedded-finance.html

[5] https://www.weforum.org/stories/2025/04/embedded-finance-disruptive-force-financial-institutions/

[6] https://fintech-alliance.com/news-insights/article/astra-tech-s-quantix-secures-500-million-for-regional-expansion

[7] https://www.weforum.org/stories/2025/04/embedded-finance-disruptive-force-financial-institutions/

[8] https://www.hsbc.com/news-and-views/news/media-releases/2023/hsbc-announces-plans-for-new-joint-venture-with-tradeshift

[9] https://thefintechtimes.com/are-traditional-banks-keeping-up-with-embedded-finance-or-are-they-falling-behind/

[10] https://www.mingzulu.com/post/embedded-finance-2024-mena-market-map

[11] https://fintechnews.africa/43597/fintechafrica/mena-companies-embrace-embedded-finance/

[12] https://www.stc.com.sa/content/stc/sa/en/personal/devices/purchasing-services/Tamara.html

[13] https://www.researchandmarkets.com/report/united-arab-emirates-embedded-finance-market

[14] https://fintechnews.ae/24289/fintechdubai/careem-pay-expands-remittance-service-to-18-more-european-countries/

[15] https://kf.gov.ae/en/news/new-phase-of-the-young-investor-program-targets-50-schools-and-more-than-75-000-students-across-dubai

[16] https://www.weforum.org/stories/2025/04/embedded-finance-disruptive-force-financial-institutions/

[17] https://www.pathward.com/news/how-embedded-finance-is-transforming-the-world-of-consumer-banki

Added to press kit

Added to press kit