The financial services sector is the oil that turn the wheels of the global economy – speedily, and with as little friction as possible. Together, financial services comprise the matrix of solutions that facilitate income, growth, risk management and – increasingly – inclusion around the world. From the macro-scale (helping nation states grow GDPs to improve living standards) to the micro (helping smallholder farmers in emerging economies buy seeds) financial services are the invisible forces that keep human society functioning.

Yet financial services, like many aspects of our interconnected 21st Century lifestyle, are on the cusp of great change thanks to dramatic advances in technology, not least Artificial Intelligence (AI). This radical technology presents us with an unprecedented opportunity to make our economic ecosystems truly fit for the future.

Research suggests 59% of finance leaders now report the deployment of AI within their businesses, a sharp rise from 37% just two short years ago.[1] Confidence in the industry is high: Two-thirds of finance professionals are feeling more hopeful about its potential for the sector than they were only a year ago, with optimism increasing among those further along the AI adoption journey.

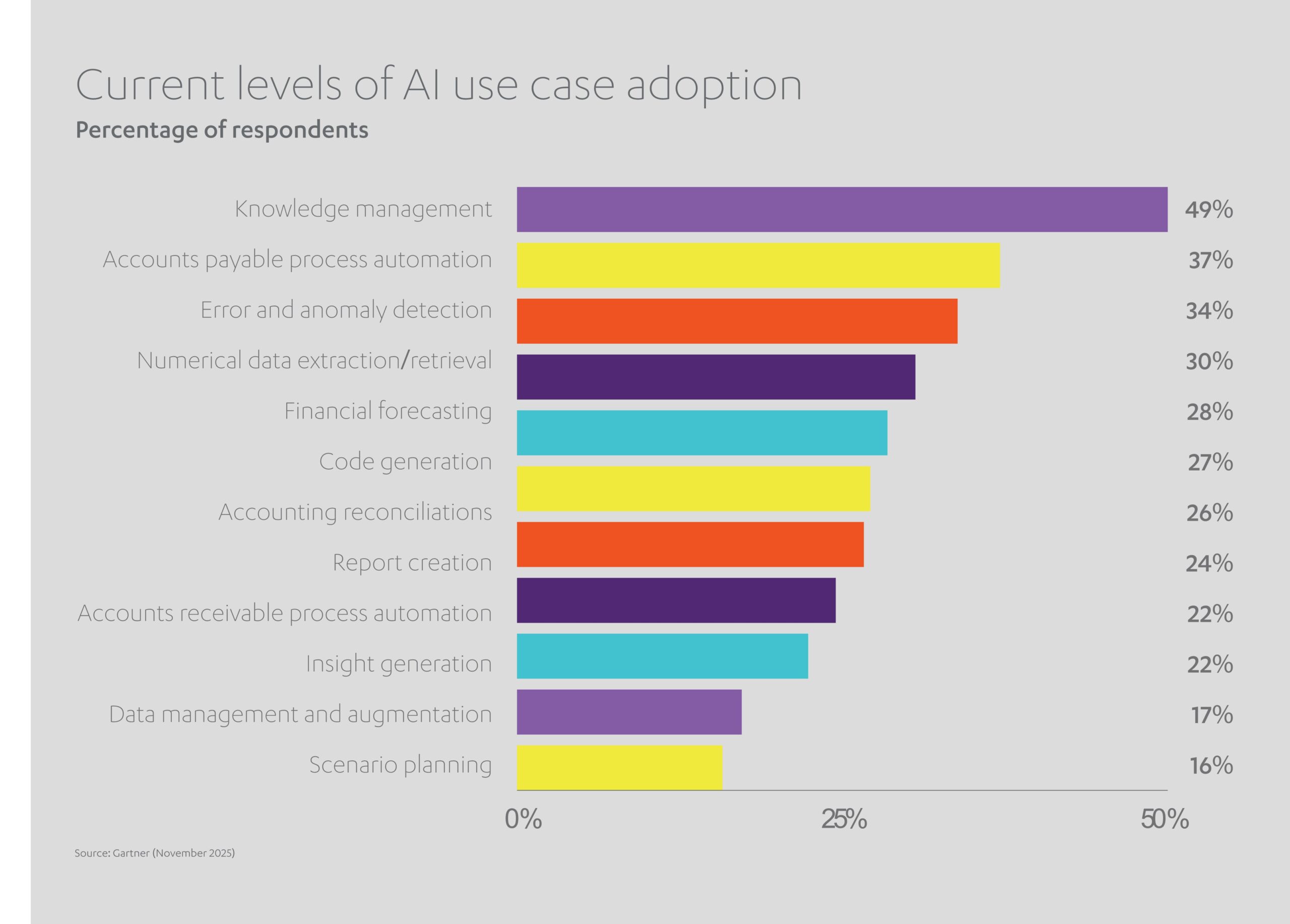

AI’s versatility – its ability to learn and diversify its skillset to straddle multiple disciplines – has seen it unleashed on a range of financial services tasks: From smarter investments and faster loan approvals, to risk reduction and future forecasting. Within the sector, industry insiders are already integrating AI across a range of workstreams, principally:

- Knowledge management (parsing data for optimized decision-making): 49%

- Automating accounts payable processes: 37%

- Error and anomaly detection: 34%

- Numerical data retrieval: 30%

- Predicting financial performance: 28%

- Code generation: 27%

Advanced generative AI (Gen AI), in particular, is growing quickly across financial services, with one-third of firms already using it as of 2025, and many more deep in the development phase.[2] Gen AI can automate myriad tasks critical to the sector which until recently demanded direct human involvement: Financial analysis, asset management, procurement, even reporting obligations.

With such power at their disposal, financial services leaders are set to turbocharge AI adoption and investment. By the end of 2026 some 90% of finance teams worldwide will operate at least one AI-driven tool.[3] Together, financial services firms are expected to funnel more than US$ 87 billion annually into AI by 2029, compared to just over US$ 18 billion in 2024.[4] The banking sector alone is expected to account for 20% of all global investments in AI by 2028 as stakeholders try to establish a competitive advantage over rivals.[5]

Against this backdrop it is easy to see why financial technology (fintech) is fast emerging as the biggest disruptors the financial services sector has ever witnessed.

How will fintech change the equation for financial services?

Whether it’s innovating new delivery models, responding to regulatory changes, or finding new ways to improve the customer experience, digital technologies are rapidly reinventing the entire value chain of financial services. Products, systems and business models that have worked for decades no longer suffice in our digitally-enabled world.

It is not just AI algorithms, with their uncanny ability to identify behavior patterns across billions of transactions, that we need to accommodate. We must also consider the implications of big data, the ‘internet of things’, blockchain technologies and cloud computing.

- Big data: Financial services providers now have more insights into customers’ lives than ever before – their habits, spending preferences, expected behaviors and credit legacies.

- Internet of Things (IoT): Sensors and connected devices, from wearable tech to home appliances, generate reams more data about consumers’ work, leisure and retail profiles.

- Blockchain: Distributed ledger technology (DLT) allows vast swathes of live data to be shared safely and securely between disparate business networks, bringing cost savings, speedier transactions and improved transparency.

- Cloud computing: Remote repositories of vast computational power offer enhanced security, personalized customer experiences like robo-advisors, and resilient disaster recovery options.

Inevitably customer expectations have evolved in parallel with these technological leaps forward. Increasingly, consumers are demanding tailor-made products and real-time financial transactions, to say nothing of decisions on loans being processed in minutes rather than days.

The technological transformation will trigger benefits for both parties, customers and providers alike:

- Lower costs: Online payments and money transfers can be approved and actioned without human intervention, saving time and money.

- Enhanced transparency: Cutting-edge technologies like blockchain can establish a provable – yet paperless – trail of transactions, safe from hackers and illegal data gatherers.

- Faster innovation: By exploiting big data, firms can nimbly respond to market trends and rapidly bring new products to market.

- Bespoke services: Customized deals and unique offers can be offered to each user in the value chain.

- Fraud prevention: Deep insight into consumer behavior can instantly flag-up suspicious activity.

- Lower risk: Algorithms can identify destructive spending patterns, potentially preventing customers falling behind with payments or taking on too much debt.

Little wonder than investments in fintech are surging. The global fintech market (companies providing financial technology services and tools to other businesses) is expected to reach US$ 460.76 billion in 2026, up from US$ 394.88 billion in 2025, and is forecast to accelerate further to US$ 1.76 trillion by 2034.[6]

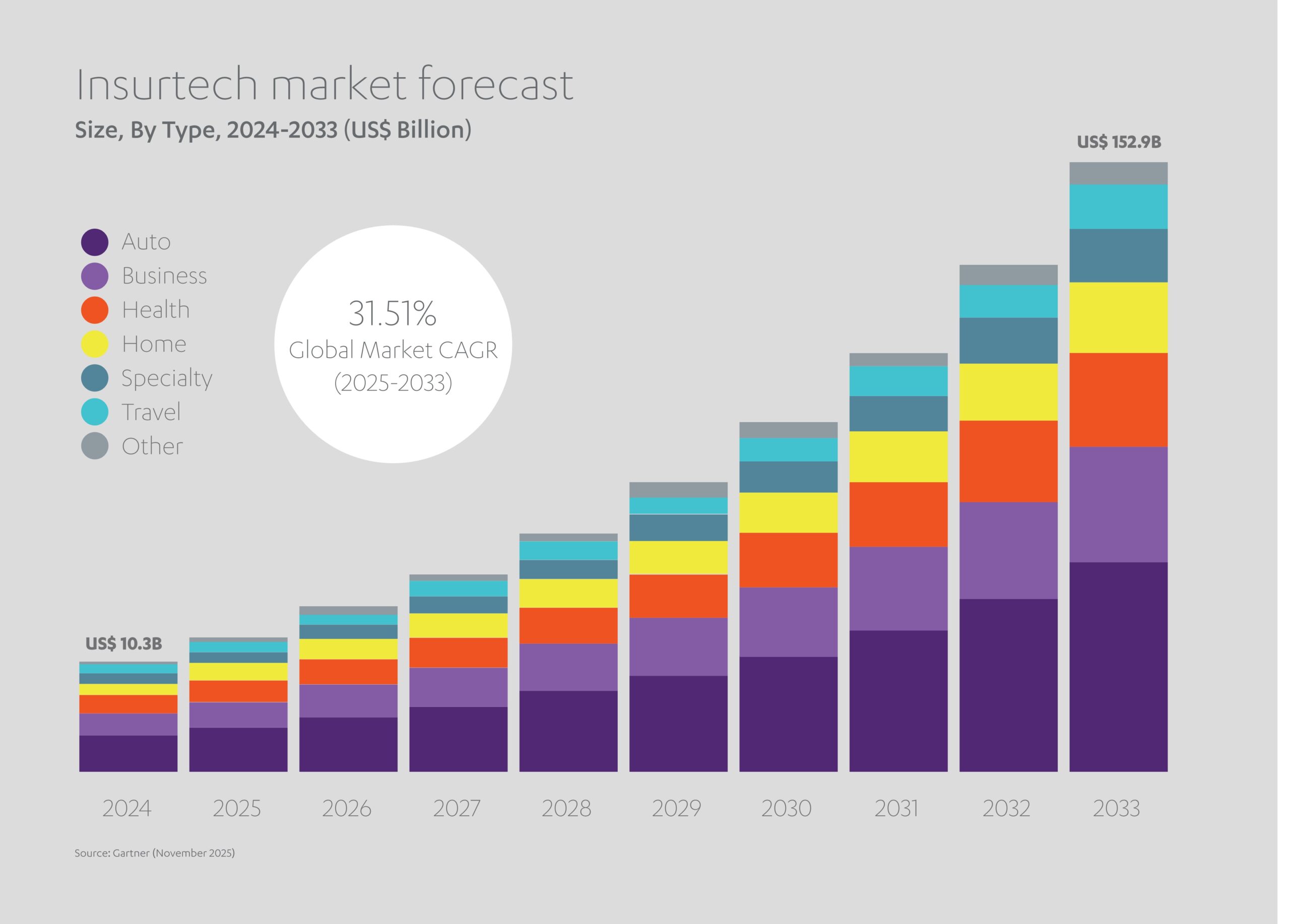

With more capital changing hands than ever before, both domestically and cross-border, how do we manage risk amid rising complexity? Arising in tandem with fintech is its investment security equivalent: Insurtech.

How is Insurtech reshaping the insurance sector?

The insurance sector has been transformed over the past decade by the democratization of data, its customer base now numbering in the billions. Anyone with access to a smartphone can quickly secure bespoke insurance cover for their homes, businesses and even lives. It’s all thanks to a digital marketplace driven by insurtech innovations, each facilitated by those critical fintech breakthroughs: AI, big data, blockchain technology, and ever-expanding 5G networks.

The torrent of personalized data from a global abundance of web-ready smart devices is helping insurtech upend the insurance industry. The ability of AI algorithms to analyze a wealth of personalized insights is helping quantify data-driven risk with more accuracy than ever before, signaling the advent of more tailormade and affordable policies. Blockchain, with time-stamped records of payments and policy inception dates, is proving indispensable for compliance, while 5G connectivity offers real-time interaction between consumers and insurance providers.

Together, insurtech is making low-risk underwriting, on-the-spot purchasing and even AI-driven claims processing a reality, helping to redefine the customer experience from start to finish.

Hundreds of companies globally are involved in modernizing every type of admin function within the insurance world. Big names like Amazon Web Services, Oracle, DXC Technology and Capgemini are opening up the industry to ambitious new disruptors like London-based JENOA, part of the Abdul Latif Jameel network of businesses. Legacy players, meanwhile, are teaming up medium-sized SaaS (Software-as-a-Service) specialists like Pegasystems, Duck Creek, Guidewire Software and OutSystems to create an ecosystem of resources which can be accessed by insurers and agents alike.

Insurtech strengthens the levers of oversight and scrutiny too, merging mass data with deep customer insights to help tackle fraud. Insurance fraud is estimated to cost the industry more than US$ 300 billion annually in the USA alone.[7] However, Mastercard claims that by deploying AI across its systems it has helped raise fraud detection rates by up to 300% – all of which will ultimately result in more competitive premiums for customers and greater confidence for lenders.[8]

Whether one is a young delivery-driver on a zero-hours contract in America looking to insure a lease vehicle, or a self-employed entrepreneur in India seeking to protect the premises of a textiles startup, it means more opportunities to live, earn and unleash one’s full potential.

Globally in 2025 the insurtech market reached a US$ 10.3 billion valuation, a figure which could soar to US$ 152.9 billion over the next decade.[9] Factors fueling this rapid growth include rising sales of IoT devices, greater use of AI for fraud detection, and customer desire for seamless digital interactions.

Of course, by removing the virtual walls between insurers, brokers and third-party providers such as vehicle recovery firms, the exchange of data becomes by necessity much more fluid. This in returns raises questions of cybersecurity: How to protect data and ensure personal privacy within the looming digital domain?

How can we neutralize risk during digital transformation?

Digitization is key to the financial services revolution unfolding before our eyes. Yet a 2025 FBI cybersecurity report cited more than 850,000 separate incidents of online crime in a single year, with losses surpassing US$ 16 billion, up 33% from 2023.[10] Cases included a mixture of phishing, extortion, personal data breaches and cryptocurrency fraud.

Global business advisory firm Deloitte highlights technology-driven corruption as a key reputational risk to organizations during the digital transformation.[11] It notes a series of key risk areas and mitigation strategies:

- Cyber protection: Fortifying digital properties against unauthorized access and maintaining confidentiality throughout integrated systems.

- Data leakage: Protecting data integrity across an entire ecosystem during use, transfer and storage.

- Third parties: Vetting external partners for their own data integrity policies and technologies.

- Privacy: Guaranteeing that sensitive personal data concerning employees and customers includes key controls around choice and consent.

- Forensics: Presenting systems and data for scrutiny in the event of breaches.

- Regulatory adherence: Developing in-house expertise to ensure operations abide by international laws and industry-specific regulations.

- Resilience: Insulating wider systems from security failures within one component.

Robust solutions require a phased approach. Redundant technology should be routinely purged from servers. Platforms must be individually shielded against unauthorized access. Cloud computing must require multi-factor authentication (MFA) for every user. Third-party technology needs to be integrated and vetted for compatibility. Organizations need comprehensive plans for business continuity, crisis management and IT disaster recovery.

Multiple cybersecurity fears persist as we migrate ever more rapidly to the digital realm – and some could carry consequences far beyond the fate of individual businesses.

What if a self-replicating Trojan horse virus infiltrated major government servers and reversed many years of digital progress? What happens if quantum computing renders conventional cryptographic algorithms obsolete and exposes sensitive data to hackers?

One potential game-changing solution lies on the horizon: Quantum cryptography.

Rooted in the laws of physics, quantum cryptography promises methods of encrypting and transmitting secure data with unprecedented levels of security.

The still in-development technology relies on four immutable laws of physics: Particles are inherently uncertain, existing in more than one place or state simultaneously; they can be measured randomly in binary positions, with specific polarities equating to the ones and zeros of traditional computing; they cannot be measured without being altered; and they can only ever be partially rather than totally cloned.

Quantum cryptography is likely to evolve along two parallel tracks: Quantum Key Distribution (QKD) and Quantum Coin Flipping (QCF).

- Under QKD, photon light particles are transmitted along a fiber optic cable, each representing a single qubit of data. The sender uses a polarized filter to define the orientation of each photon while the receiver uses a beam-splitter to interpret that position. These matching values then become a shared key for decoding encrypted data. Any change in the quantum states of the photons will alert the users that the signal has been intercepted. QKD has been proven in the lab but is currently limited by the fact that photons sent via fiber optics degrade after several hundred miles – although ‘photon repeaters’ have recently shown promise in extending ranges.

- QCF allows two parties to conduct a randomized 50/50 test without need for external verification. It hypothesizes a ‘quantum coin’ in a superposition of states, simultaneously both heads and tails. This coin, in reality a photon particle, is prepared and sent from one party to the other, collapsing to a 1 or 0 (heads or tails) upon being measured. Relying on the fundamental randomness of the universe, it is essentially incorruptible because any attempt to interfere with the particle before its ‘reveal’ will alter its state and be instantly detectable.

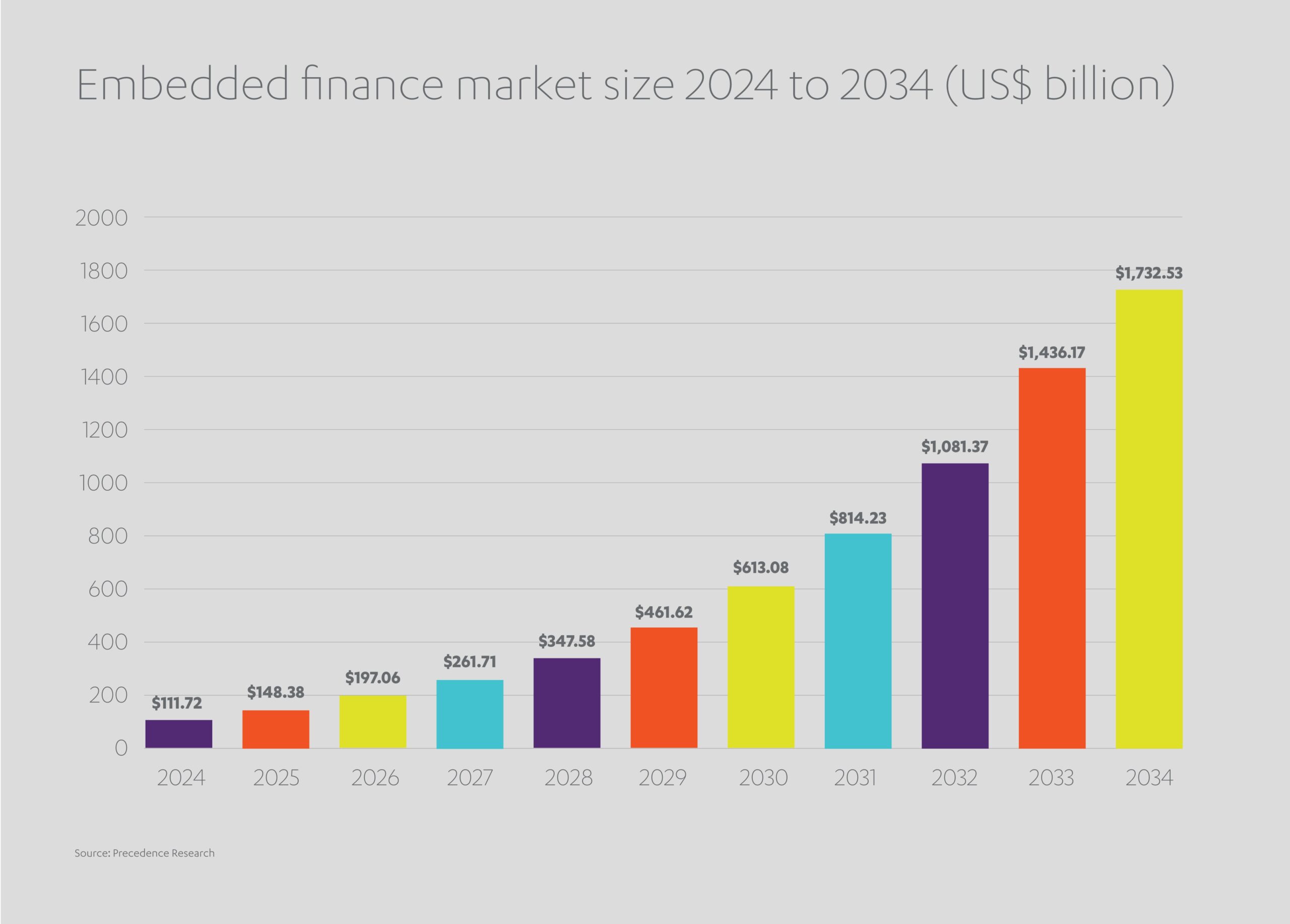

Digital technology underpins all of these advances in financial services, but the customer remains king. Increasingly, a prime motivator for interactions with commercial entities is convenience. Here, one concept above all others promises make transactions simpler and more efficient than ever before: Embedded finance.

Is embedded finance banking’s best kept secret?

Embedded finance is the ultimate expression of user-friendly design – a super-complex mesh of computational calculations, so breathtakingly simple in its final manifestation that most of us use it daily while barely noticing its presence.

Paying for train tickets through an app, buying a new outfit from an online store, or reimbursing a friend for a meal out via a digital wallet – all of these everyday activities and thousands more involve embedded finance, even though to many people the term remains obscure.

Simply put, embedded finance refers to the incorporation of everyday financial amenities – banking services, insurance, payments or loans – into nonfinancial websites and apps. This wholly interoperable software, sharing a universal language, permits customers to conduct financial transactions instantaneously through a business’s own platform rather than navigating away to a third-party provider. Speed and simplicity combine for the holy grail of convenience.

The behind-the-scenes innovation supporting this technology is an Application Programming Interface, or API, managed by an external banking-as-a-service partner. Best imagined as a software intermediary, it enables secure data exchanges between financial institutions and customer-facing apps such as retailers, banks or investment platforms.

All this unfolds with just a few button presses, or the wave of a cellphone in front of a contactless card reader. Embedded finance has emerged as a genuinely transformational financial tool, one which has undergone mass adoption and now funnels trillions of dollars between accounts worldwide.

The embedded finance market was valued at US$ 111 billion worldwide as of 2024 and is tipped to reach US$ 613 billion by 2030. The trend is truly global.[12] In the MENA region, for instance, an embedded finance market value of US$ 11.2 billion in 2024 is predicted to balloon to US$ 37.7 billion by 2029.[13]

Crucially for emerging economies embedded finance unlocks new opportunities for borrowing, from SME credit lines within e-commerce platforms, to instant personal loans accessed through consumer apps. It is another example of how the world’s new tech-powered commercial landscape is unlocking financial inclusion in developing nations once excluded from the mainstream economic system.

Will new technology liberate the financially excluded?

Access to finance is a vital prerequisite for personal progress and, in some cases, protection from poverty. From a minimum wage laborer needing food for the family table, to a single parent wanting to fund childcare so they can go out and earn, the ready flow of capital is a liberating, sometimes life-saving, force for change.

It is somewhat sobering therefore to realize that well over a billion people worldwide still lack access to a bank account, surviving day to day on whatever money they can make, without hope of ever saving for an emergency.[14]

In the absence of modern financial services, people in the developing world are unable to safeguard themselves against hardship, or invest in building a more secure future. At a broader level, entire nations miss out on the benefits of economic growth and long-term social development.

While the problem is far from eradicated, technology is beginning to have an impact on financial inclusion. Globally, around 79% of adults now have access to a banking service, an increase of five percentage points since 2021.[15] Positive changes are visible across emerging economies. Only 27% of adults in Sub-Saharan Africa had some form of mobile money account in 2021, but latest research shows this has since risen to 40%. Similarly, figures in Latin America and the Caribbean have increased from 22% to 37% over the same timeframe.

At least half of all accounts in lower-income societies are digitally-enabled via cellphones or debit cards, synching them up with banks, microfinance lenders, post offices or credit unions. Even though there is some regional variance, approximately 86% of adults worldwide now own a mobile phone, bringing at least the possibility of financial liquidity to their fingertips.[16]

The technological revolution is helping narrow the global gender gap too, with 73% of women in lower-income countries now benefiting from bank accounts, a sharp rise from just 50% a decade ago.[17] The proportion of adults in developing economies saving money each month has risen from 16% to 40% since 2001.

Financial inclusion is fundamental to many of the UN’s 17 Sustainable Development Goals to create a more sustainable future for all: No poverty, zero hunger, good health and wellbeing, access to education, gender equality, economic growth, and better industry and innovation. The private sector is playing an increasingly vital role in shaping and maintaining this exciting new economic ecosystem.

How can the private sector help fund a fairer future?

An effective, cohesive global financial system brings prosperity and opportunity to those communities most in need.

With its reputation for commercial innovation, and a range of investments across the finance spectrum, the Abdul Latif Jameel network of businesses is playing its part in securing an independent future for developing economies.

In the financial services sector, Abdul Latif Jameel is committed to investing in the people and infrastructure of the MENAT region, encouraging individuals and organizations to flourish. Businesses in Saudi Arabia, Egypt and Turkey offer bespoke financing solutions for vehicles, consumer products, commercial equipment, real estate and insurance.

Abdul Latif Jameel Finance Saudi Arabia, for example, under the leadership of CEO Dr Khalid Alsharif, recently won two prizes at the annual Monsha’at awards: ‘The Leading Non-Bank Financial Institution for MSME Funding’ and ‘The Highest Growing Non-Bank Financial Institution for MSME Funding’.

To date, Abdul Latif Jameel Finance Saudi Arabia has provided some SAR 4.2 billion in funding to more than 294,000 MSMEs[18] across key sectors including technology, manufacturing, tourism and entertainment.

Abdul Latif Jameel Finance Saudi Arabia also helps people fulfil their ambitions with a downloadable mobile cash app. The app enables customers to secure loans, without a guarantor, of between SAR 10,000 and 300,000. Applications can be approved in minutes, with flexible repayment terms spanning 12 months to five years.

Similarly in Türkiye, ALJ Finans offers customers fast, easy, and competitive financing solutions for new and used vehicle purchases through its automotive partners, and supports the cash flow of its business partners with its inventory financing service, while its ALJPay app simplifies access to products, credit applications, payments, and follow-up processes.

Meanwhile, the Abdul Latif Jameel Investment Management Company (JIMCO), the global investment arm of the Jameel Family, is making it easier for countless businesses to access vital finance.

JIMCO has invested, for example, in buy-now-pay-later fintech startup Tabby, helping customers across the UAE and Saudi Arabia pay for purchases via deferred payments at no extra cost; Figopara, in Türkiye extending working capital to businesses by lengthening payment terms to suppliers; Thndr, a mobile-first equities trading platform allowing individuals to make commission-free investments in stocks, bonds and funds; Rain, giving investors in the Middle East access to cryptocurrency markets; and Lean, a B2B platform designing software for securely connecting financial services institutions to customer bank accounts.

“Financial services are at a technologically-driven inflection point,” says Fady Jameel, Vice Chairman, International, Abdul Latif Jameel. “The decisions we take now will impact access to finance, economic security and data integrity for many decades ahead.

“We have at our disposal a suite of ever-more versatile tools to manage the flow of capital around the world. We must ensure they are deployed widely and wisely, and with core imperatives at heart: Unleashing innovation, increasing fairness and freedom, and securing a more prosperous world for generations to come.”

Financial services: Five fast facts

Q: How widely used is AI among finance professionals?

A: 59% of finance leaders are now rolling out AI within their businesses, a sharp rise from 37% just two years earlier.

Q: How rapidly are fintech investments rising worldwide?

A: The global fintech market, expected to reach US$ 460.76 billion in 2026, is forecast to accelerate to US$ 1.76 trillion by 2034.

Q: Can fintech help solve the problem of insurance fraud?

A: One payment card operator notes that deploying AI across its systems has helped raise fraud detection rates by up to 300%.

Q: Is embedded finance set to be a runaway success?

A: Valued at US$ 111 billion in 2024, the embedded finance market is tipped to reach US$ 613 billion by 2030.

Q: Is digitization helping to democratize access to finance worldwide?

A: Globally, around 79% of adults now have access to a bank account, 5% more than in 2021.

[1] https://www.gartner.com/en/newsroom/press-releases/2025-11-18-gartner-survey-shows-finance-ai-adoption-remains-steady-in-2025

[2] https://asianbankingandfinance.net/banking-technology/in-focus/banks-ai-adoption-shape-cost-and-revenue-advantage

[3] https://electroiq.com/stats/ai-in-finance-statistics

[4] https://www.globenewswire.com/news-release/2025/11/25/3194418/0/en/AI-in-Financial-Services-Strategic-Intelligence-Report-2025-Opportunities-in-Enhancing-Cybersecurity-and-Fraud-Prevention-Automating-Complex-Workflows-and-Improving-Decision-making.html

[5] https://asianbankingandfinance.net/banking-technology/in-focus/banks-ai-adoption-shape-cost-and-revenue-advantage

[6] https://www.fortunebusinessinsights.com/fintech-market-108641

[7] https://www.pwc.com/gx/en/industries/financial-services/insurance/financial-crime-in-the-insurance-industry.html

[8] https://www.globenewswire.com/news-release/2025/11/25/3194418/0/en/AI-in-Financial-Services-Strategic-Intelligence-Report-2025-Opportunities-in-Enhancing-Cybersecurity-and-Fraud-Prevention-Automating-Complex-Workflows-and-Improving-Decision-making.html

[9] https://www.imarcgroup.com/insurtech-market

[10] https://www.fbi.gov/news/press-releases/fbi-releases-annual-internet-crime-report

[11] https://www.deloitte.com/in/en/services/consulting/services/deloitte-forensic.html

[12] https://www.precedenceresearch.com/embedded-finance-market

[13] https://www.weforum.org/stories/2025/04/embedded-finance-disruptive-force-financial-institutions/

[14] https://openknowledge.worldbank.org/entities/publication/8b9002b6-d8dd-426c-aa7c-6d7d16902cd7

[15] https://openknowledge.worldbank.org/entities/publication/8b9002b6-d8dd-426c-aa7c-6d7d16902cd7

[16] https://openknowledge.worldbank.org/entities/publication/8b9002b6-d8dd-426c-aa7c-6d7d16902cd7

[17] https://openknowledge.worldbank.org/entities/publication/8b9002b6-d8dd-426c-aa7c-6d7d16902cd7

[18] Micro, Small & Medium Enterprises

Added to press kit

Added to press kit